Articles

Best Payment Processor for Small Business in Qatar: The Definitive SADAD Guide

You want to start taking payments. Today. You sell through WhatsApp, Instagram, or a simple site. You need local cards to work. You need a clean checkout. You need a live dashboard that tells you what got paid.

to find the Best Payment Processor

SADAD is the straight path.

This guide gives you a clear plan to go live fast. No website required.

What you’ll get:

- How to create a payment link and get paid in minutes.

- How to send invoices your customers can pay on WhatsApp or email.

- How to accept Visa and Mastercard, in addition to Qatar debit cards through NAPS and QPay.

- How to add Apple Pay when your bank supports it.

- How to connect SADAD to WooCommerce or Shopify with ready plugins.

- What to check on pricing, settlement, and refunds before you switch on.

Read this if you want a setup that works now and scales with you later.

Payment’s fundamentals: what every small business in Qatar should know

Best Payment Processor

Before we talk tools, you need a clear picture of how money moves online in Qatar. Once you see the flow, every setup decision gets easier.

The key players

- Cardholder – your customer.

- Merchant – you.

- Acquirer/processor – the party that routes card data to the networks and back.

- Issuing bank – your customer’s bank. It says yes or no.

- Gateway/PSP – the secure front door that collects card details and returns a result to your site or link.

One provider can bundle several of these roles. That’s fine. What matters is that the provider speaks Qatar’s rails and gives you clean reporting.

The Qatar online flow (what your buyer actually sees)

A customer enters card details on your checkout or invoice link. They get a one-time password by SMS. They confirm with their card PIN on the bank page.

You show a clear success state. Your dashboard updates within seconds.

That two-step check – OTP then PIN – is normal in Qatar. It builds trust and lifts approval rates. Plan your copy around it so no one gets confused.

Fees in plain terms

Every online card payment carries network costs. Two big pieces drive most of it:

- Interchange – goes to the issuing bank. It covers risk and card program costs.

- Network fees – go to the card networks. Think authorization and cross-border costs.

Your effective rate depends on card type, channel, and your mix of domestic vs international. Don’t guess. Ask for a blended estimate based on your last 30 days of sales or a realistic forecast if you’re new.

For all small businesses accepting online payments in Qatar

This part covers what every business needs to get right: the funnel that drives conversion, the checkout choices that cut drop-off, the basics of risk, and the signals that lift bank acceptance. Read this section first. Then jump to the playbooks that match how you sell.

The funnel that decides your revenue

Every payment passes three gates: checkout completion, risk checks, bank acceptance.

Conversion happens only when all three say yes.

- Checkout completion: did the buyer finish the form or the invoice link.

- Risk checks: did obvious fraud get stopped without blocking good buyers.

- Bank acceptance: did the issuing bank approve the charge.

Your job is to tighten all three. Treat them as one system, not separate projects.

Create a checkout that finishes the job

Short forms win. So does clarity.

- Keep fields lean. Name, email, phone when needed, card details.

- Make the OTP + PIN step obvious. Tell buyers they’ll see their bank page and confirm there.

- On mobile, surface Apple Pay when your bank supports it. It removes manual entry.

- Use responsive layouts and a numeric keypad for card inputs.

- Load fast on 4G. Every extra second drops paid conversions.

If you sell by link or invoice, the same rules apply: clear amount, tight description, one clean pay action, success state that’s impossible to miss.

Manage risk without killing approvals

The goal is not zero fraud. The goal is low fraud with high acceptance.

- Start with simple rules: block obvious abuse, cap risky amounts, flag mismatched emails.

- Add signals over time: velocity, device fingerprint, past disputes.

- Avoid blanket bans that nuke good buyers.

- Review edge cases weekly; tune, don’t overfit.

When you need stronger checks, use step-up prompts only where risk is real, not on every transaction.

Lift bank acceptance

Issuing banks say yes or no based on data quality and account status. Give them clean signals.

- Pass CVC, name, email, and billing details when available.

- Use a clear statement descriptor buyers will recognize.

- Retry soft declines with intent, not loops; space attempts and vary authorization data where allowed.

- In Qatar, design around the QPAY path: OTP by SMS, then PIN on the bank page. Set expectations in your copy and test the return to your success screen.

Offer the methods that actually move the needle

Cards are your base. Local rails matter.

- Accept domestic debit on the national rails with the QPAY flow.

- Add Apple Pay for mobile buyers when your bank supports it.

- Keep payment links and invoices ready for WhatsApp and email flows. They close sales without a website.

Keep tax and invoicing simple

VAT and invoicing rules change by jurisdiction. Build habits that scale.

- Use sequential invoice numbers and clear tax lines.

- Export reports that map to your accounting fields.

- Reconcile settlements by day; test a full refund and a partial refund before you need them.

What this section gives you: a mental model for payments that matches how Qatar actually works. Next, we’ll apply a scoring lens to SADAD so you can make fast, confident decisions about setup, plugins, and day-one execution.

What we evaluate and how we score SADAD

This is the decision lens. When a small team asks for the best processor, I score five things that move cash to your account with the least friction.

The scoring weights

- 30%: Time to first payment: From sign-up and basic KYC to a real card charge. Same day is the bar.

- 25%: Local acceptance: Support for Qatar’s rails. Buyers expect the QPAY path: OTP by SMS, then PIN on the bank page.

- 20%: Sell without a website: Links and invoices you can share on WhatsApp or email. Live status. Reminders that actually get paid.

- 15%: Plugins and API: A clean WooCommerce path, a documented route for Shopify, and an API you can build on later.

- 10%: Reporting, refunds, and controls: Real-time view of paid vs unpaid, one-click refunds, exports that match your accounting fields.

How I test this in the real world

- Open a merchant account and complete basic KYC.

- Create a payment link and an invoice. Pay both with a domestic debit card.

- Walk through the full QPAY flow and confirm the return to your success page.

- If you have a store, install the WooCommerce plugin or follow the Shopify guide, then place a low-value live order.

- Trigger one full refund and one partial refund. Confirm both in the dashboard and in store admin.

- Export reports and check column mapping for tax, reference, and order ID.

- On mobile, test Apple Pay if your bank supports it. Look for a faster path on iOS without breaking the card flow.

SADAD against the rubric

Time to first payment: strong. Create a link or invoice from the dashboard and collect a real payment the same day. No site required.

Local acceptance: strong. Built for Qatar’s checkout reality. The copy and flow expect OTP by SMS and PIN on the bank page.

Sell without a website: strong. Links and invoices are shared cleanly on WhatsApp and email. Status updates in real time with simple reminders.

Plugins and API: strong. Native path for WooCommerce, a documented route for Shopify, and a developer hub with APIs, SDKs, and webhooks.

Reporting, refunds, and controls: strong. Live transactions, quick refunds, clean exports. Finance gets the data it needs without manual cleanup.

What this means for you

- You can take a real payment today with a link.

- You can accept domestic debit on the rails buyers trust.

- You can keep selling in DMs while your store takes shape.

- You have a clear path to WooCommerce and Shopify when you’re ready.

- Your reports and refunds behave the way a business needs them to.

Next, you’ll see SADAD at a glance: the specific actions you can launch this week and the problems each one solves.

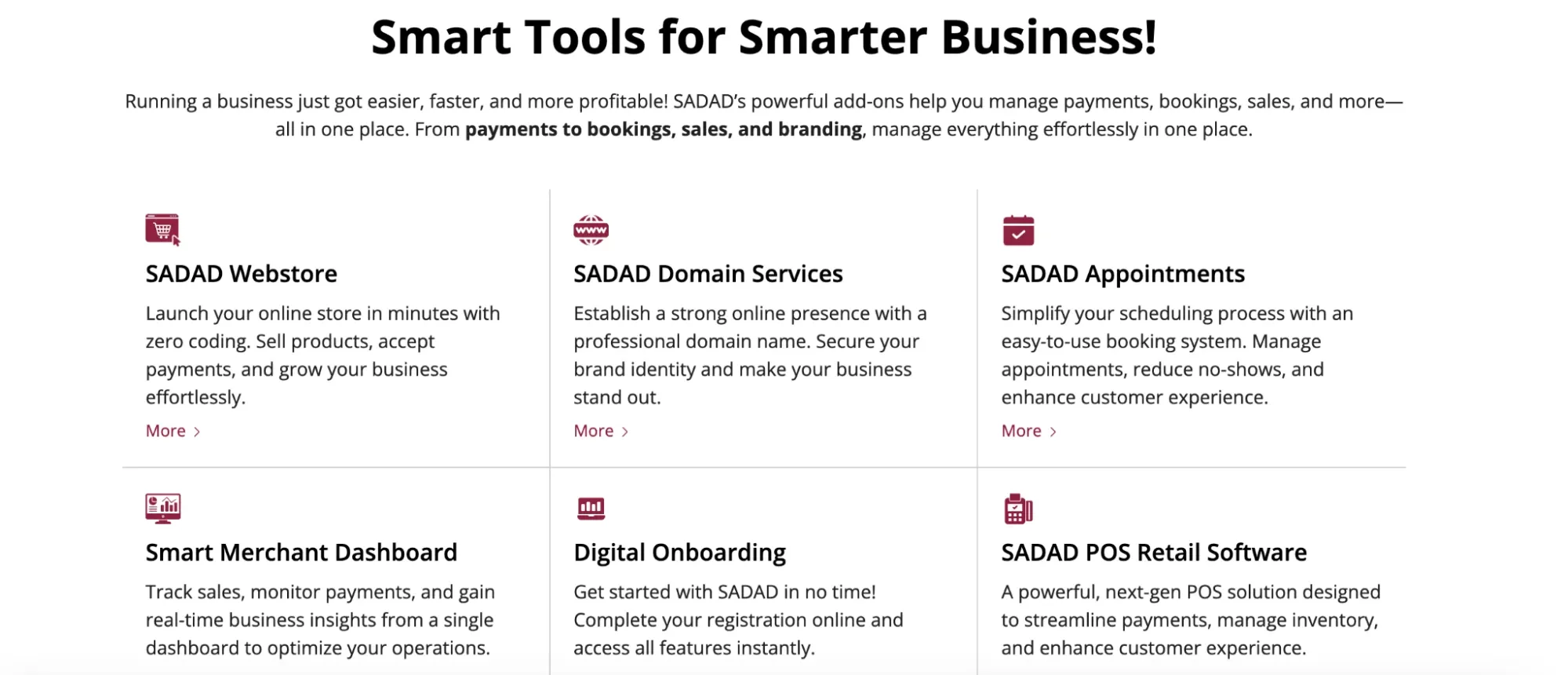

SADAD at a glance: what you can launch this week

You want outcomes, not a feature catalog. Here is what you can turn on now and what each piece does for your revenue.

Payment links you can share anywhere

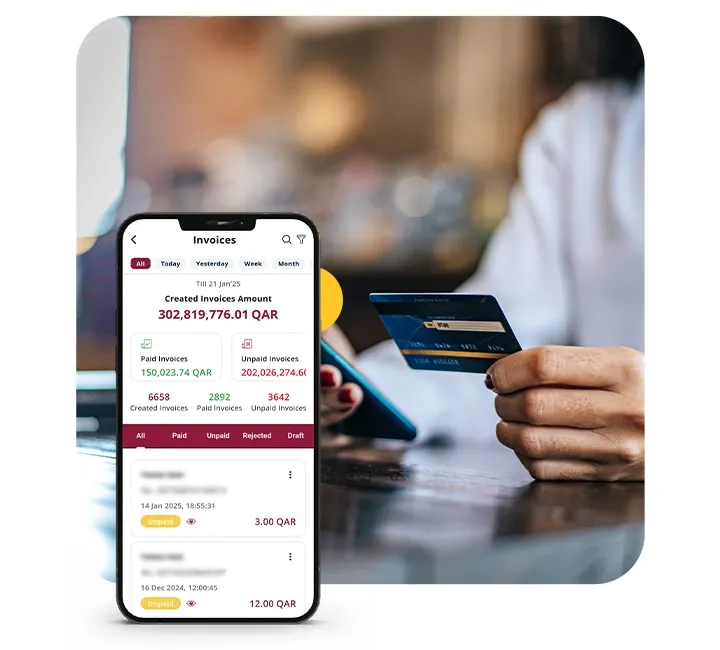

Create a link in the dashboard, add amount and description, hit generate. Share it on WhatsApp, SMS, or email. Track opened, paid, and failed in real time.

Why it matters: you sell without a site, close DMs faster, and prove demand before you invest in a full store.

Payable invoices that get settled

Build an invoice with line items, tax, and a due date. Each invoice includes a pay button. Send by email or paste the link into WhatsApp. Set reminders for due and overdue.

Why it matters: you stop chasing transfers and turn service work into predictable cash flow.

Product links for social selling

Use Tarweej to generate a link per product. Drop it in bios, stories, and DMs. Buyers move from discovery to payment without extra steps.

Why it matters: you convert attention into orders with fewer clicks.

Built for Qatar’s checkout reality

Support the QPAY flow for domestic cards. Buyers receive an OTP by SMS and confirm with their card PIN on the bank page. Write a clear copy that sets this expectation and test the return to your success screen.

Why it matters: trust rises, approval rates follow.

Apple Pay on mobile when your bank supports it

Surface Apple Pay on iOS for one-tap checkout. Keep card rails as the default for maximum coverage.

Why it matters: you lift mobile conversion without breaking the base path.

Plugins and developer path

WooCommerce: install the SADAD QA Payment plugin and enable Pay with SADAD. Shopify: follow the merchant guide to add a custom method. Developers: use the API, SDKs, and webhooks to extend flows or add native apps.

Why it matters: you start simple and keep a clean path to scale.

Dashboard, reporting, and refunds

See transactions as they happen. Trigger full or partial refunds from the same screen. Export reports that map to your accounting fields.

Why it matters: finance gets clarity, customers get fast resolutions.

What this solves right now

- Take your first payment by link in minutes.

- Send invoices that get paid on time.

- Accept domestic debit on the rails buyers expect.

- Keep a smooth route to WooCommerce and Shopify without custom code.

Next section: setup playbooks for links, invoices, WooCommerce, Shopify, and mobile so you can go live step by step.

Setup paths for small businesses in Qatar

Pick the setup that matches how you sell. I’ll explain why it works, what to watch, and how to keep a clean path to scale.

Selling without a website: links first, cash soon

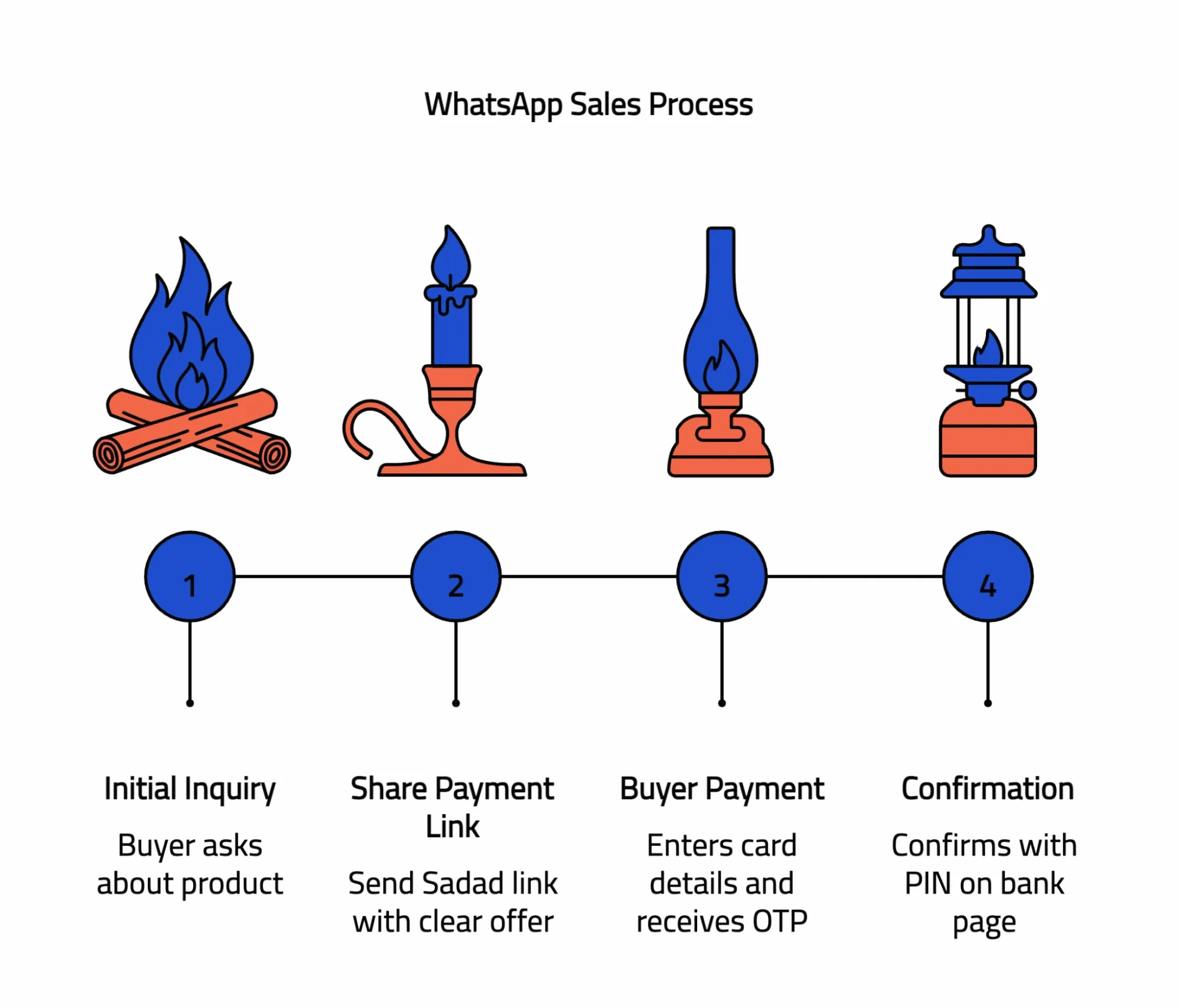

Payment links are the fastest way to prove demand. You create a link in the dashboard, share it on WhatsApp or email, and watch the payment land. The buyer sees a clear amount and purpose, then moves through Qatar’s familiar path: OTP by SMS followed by PIN on the bank page. That two-step flow builds trust. It also reduces “I wasn’t sure it went through” messages.

What makes links convert:

- A tight description that matches what the buyer expects to pay.

- Plain copy that explains the OTP and PIN step before it appears.

- A success state that is obvious and loads quickly on mobile.

When to outgrow links: once you repeat the same offer daily, or you need inventory, taxes, and shipping rules on autopilot. Until then, links are the right speed.

Services and projects: invoicing that actually gets paid

If you sell time, packages, or one-off deliverables, invoices beat bank transfers. Each invoice includes a pay button and tracks status. You keep numbering consistent for accounting, show tax lines, and send reminders automatically. Think of it as your payment page wrapped around a professional document.

How to keep invoicing clean:

- One invoice per scope with a clear reference that buyers will recognize later.

- Due dates that match your workflow. Use deposits when you need commitment.

- A small test refund before you need a real one, so you know the path.

Invoices do more than collect money. They reduce back-and-forth, make reconciliation predictable, and let you hand clean exports to finance.

WooCommerce on WordPress: native checkout, minimal friction

Many small stores in Qatar choose WooCommerce because it is flexible and familiar. The goal is a native payment method that feels like part of your store and respects the local flow. With the SADAD plugin, you keep shoppers in your brand, pass clean order references, and issue refunds from the same admin they already use.

What matters most here:

- Mobile behavior. The cart to checkout handoff must be instant on 4G.

- Order integrity. The payment reference should attach to order notes for easy support.

- Caching rules. Exclude checkout and thank-you pages so the return from the bank page never breaks.

If you keep those three in shape, you get a checkout that feels first-party and a back office your team understands.

Shopify: keep your theme, add Qatar-ready payments

Shopify gives you speed, themes, and a tight admin. Your job is to add a card method that speaks the local rails without disturbing the buying flow. Follow the merchant guide, create the connection, and limit availability to Qatar if you sell locally. Place a live order, read the order timeline, and make sure the payment reference appears where support will look.

Two practical checks:

- The thank-you page should load immediately after the bank page, with no extra taps.

- Abandoned checkout flows should still fire if a buyer drops before the bank page.

If both are true, you have a shop that converts on mobile and keeps all the operational signals in one place.

Mobile apps and custom builds: go native the right way

Apps win when the payment feels like part of the product, not a detour. That starts with a server-first approach. Create payments on your backend, never expose keys in the app, and use tokenization for returning buyers. Webhooks carry the truth of paid, failed, and refunded. Treat them as a source of record and make handlers idempotent so repeats never double-charge.

Architecture that scales:

- A dedicated service for payments with clear logs and correlation IDs.

- A retry path for soft declines and timeouts that respects the user experience.

- A tested return from the OTP and PIN page to the exact screen the user expects.

Do this now and you avoid rewrites when volume climbs.

Pricing, settlement, and risk: confirm the money path

Good setups die when money is unclear. Lock down the basics early. Ask for an effective rate that reflects your mix of domestic and international cards. Write down settlement timing and any reserves. Know the chargeback fee and the dispute window. On day one, run three transactions: a live charge, a full refund, and a partial refund. Export reports and check that columns map to your accounting fields.

What you gain:

- Forecastable costs.

- Faster support responses when you quote exact references.

- Confidence that refunds and disputes won’t surprise you later.

This is how you move from idea to working payments without turning your week into a build. Links prove demand. Invoices clean up service work. WooCommerce and Shopify bring structure when you need a store. Custom flows stay safe when the server owns the keys and webhooks tell the truth.

Next, we will map these setups to real scenarios in Qatar and show what to measure in week one.

Real-world scenarios in Qatar

Small businesses win when payments fit how people actually buy. The examples below show what that looks like with SADAD. Read the one that matches your week. Borrow what works. Keep moving.

Selling through WhatsApp and Instagram

You start with a conversation. A buyer asks for a price or a size. You answer, then share a SADAD payment link with a clear label and amount. The buyer sees a clean page, enters card details, receives an OTP by SMS, confirms with a PIN on the bank page, and lands on your success screen. No store required. No detours.

Two things drive results here. First, clarity. Name the offer in the link so the buyer recognizes it in one glance. Second, pace. Send the link while the chat is warm and follow with a short reminder if it stalls. Over a week, you’ll see a pattern: links close impulse buys fast and turn DMs into a repeatable sales lane.

What to watch: the share of clicked links that become paid, mobile load time on 4G, and how often buyers ask, “Did it go through?” If that question pops up, add one sentence above the pay button that explains the Qatar flow: OTP by SMS, then PIN on the bank page.

Services, coaching, and one-off projects

If you sell time or deliverables, invoices do more than collect. They set terms. A SADAD invoice carries line items, tax, and a due date along with a pay button. You send it by email or paste the link in WhatsApp. The system tracks opened and paid so you are not guessing.

This format reduces friction on both sides. Clients see a professional document with everything in one place. You keep numbering consistent for accounting and trigger reminders without chasing. Do one dry run on a small amount so you know the refund path before you ever need it.

The metric that matters is days to payment from send. If it stretches, tighten scope descriptions and use deposits to create commitment. Most service businesses see fewer disputes once invoice references match how finance files work.

WooCommerce on WordPress

Many shops in Qatar use WooCommerce for its control and familiarity. Your goal is a checkout that feels native and respects local rails. With the SADAD plugin enabled, shoppers remain in your brand, orders carry the SADAD reference in the notes, and refunds happen inside the same admin your team already knows.

The make-or-break details live on mobile. Cart to checkout has to hand off instantly. Return from the bank page must land on a clear thank-you view. Exclude checkout and thank-you URLs from caching so nothing gets stuck. When these pieces are in place, you get fewer abandoned sessions and cleaner support work because every order shows the payment reference where staff can find it.

As volume grows, add Apple Pay if your bank supports it. It helps iOS buyers finish faster without changing the base card path.

Shopify

Shopify gives you speed, themes, and a tidy back office. Your task is to add a card method that speaks Qatar’s flow while keeping the buying experience smooth. Follow the SADAD merchant path to set up a custom method, scope it to Qatar if you sell locally, and place a live test order.

Read the order timeline. You want the SADAD reference recorded where support will look. Then check the two failure points that cost stores the most: a slow handoff to checkout and abandoned flows that stop sending emails after the bank page. Fix those and you preserve both conversion and recovery.

Mobile apps and custom builds

In apps, payments should feel like part of the product. That starts on the server. Create payments on your backend, hold keys out of client code, and use tokenization for returning buyers. Webhooks are your source of truth. Handle paid, failed, and refunded with idempotent logic so retries never double-charge.

Design around the Qatar step. After OTP and PIN on the bank page, return users to the exact screen they expect with a visible success state. Add a gentle retry for soft declines and log the SADAD transaction reference alongside your order ID. When you ship this way, you keep trust high and support simple even as traffic grows.

What to measure in week one

Pick a few signals and learn fast. Time to first payment from sign-up. Acceptance rate on domestic debit. Link click-to-pay for WhatsApp sales. Refund resolution time. Report accuracy against your accounting fields. If one number looks off, fix that path first. Clean money flows beat new features every time.

Pricing, settlement, and risk in practice

Payments aren’t just a button on your site. They are contracts, costs, and timelines that shape cash flow. Before volume arrives, get clear on how money moves through your stack.

Start with pricing you can predict. Every card transaction carries network costs that vary by card type and channel. Your goal is a single effective rate you can plan around. Ask for a number that reflects your actual mix of domestic debit and international cards, not a headline you never see in practice. Then map where fees land. Some providers deduct on each charge. Others net them on settlement. The difference shows up in your bank reconciliation.

Settlement timing matters as much as price. Daily, two-day, or weekly cycles change when you can restock or run ads. Write down cut-off times and holiday rules. If a rolling reserve applies, record the percentage and release schedule so finance isn’t guessing. Pair this with a payout report that lists every charge and refund in each settlement. That report is your source of truth when the bank statement arrives.

Risk is the third leg of the stool. In Qatar, buyers expect to receive an OTP by SMS and confirm with their card PIN on the bank page. Say that on your checkout. Clarity reduces drop-off and disputes. Keep a recognizable statement descriptor so customers see your name on their bank app. When a chargeback happens, treat it like operations, not drama. Know the fee, the evidence window, and the exact path to submit proof. Test refunds on day one so support never stalls.

A simple drill closes the loop. Run one live charge, one full refund, and one partial refund. Export a payout report, reconcile it to your bank, and save the steps. That routine is worth more than any feature list because it protects cash and time.

Choosing a starting path

The best setup is the one that matches how you sell today and grows without rework. If you sell through conversations, start with payment links. They turn WhatsApp and email into revenue without a storefront. If you invoice for services, switch bank transfers for SADAD invoices and let reminders do the follow-up. When a catalog appears and orders repeat, WooCommerce gives you a native checkout that fits your brand. Shopify gives you speed and a tight admin. Both keep a clean route to Qatar’s card flow.

Mobile apps sit on a different axis. Here, the payment should feel like part of the product. Create charges on your server, hold keys out of client code, and use tokenization for returning buyers. Webhooks tell you what actually happened. Treat them as the ledger and make handlers idempotent so retries never double-charge.

If two paths fit, take the one that gets you paid this week and layer the rest. Links prove demand. Stores add structure. APIs let you compose when scale arrives.

Questions small businesses ask

Do I need a full website to take payments?

No. Payment links and invoices cover day one. They let you sell from DMs, email, and simple landing pages. Build a store when your catalog and logistics need automation.

How does the online card flow work in Qatar?

Buyers enter card details, receive an OTP by SMS, confirm with their PIN on the bank page, then return to your success screen. Tell them this before it happens. Trust goes up and support tickets go down.

Can I offer Apple Pay?

Yes when your bank supports it. Think of Apple Pay as a fast lane for iOS buyers. Keep card rails on by default for coverage across banks and devices.

What if a payment fails?

Treat soft declines as recoverable. Offer a gentle retry and keep a fresh link or invoice ready. Watch failures in the dashboard and follow up while intent is warm.

Can I do subscriptions later?

Yes. Start with invoices or links to validate the offer. When it stabilizes, move recurring charges to the API with tokenization and webhooks so renewals stay accurate.

How do refunds appear?

You issue them in the dashboard or your store admin. They attach to the original transaction, appear in payout exports, and post back to the buyer after the card network processes the reversal.

What should finance receive each month?

A payout report that ties settlements to charges and refunds, invoice exports with numbering and tax lines, and an up-to-date list of disputes with due dates. That package closes books without guesswork.

Before we wrap up.

Payments glossary for small businesses in Qatar

You will see these terms in dashboards, bank emails, and support threads. Keep this list close. It turns jargon into decisions.

- Authorization: the bank’s yes or no on a payment attempt.

- Capture: when a successful authorization becomes money owed to you.

- Acquirer: the bank or partner that routes your transactions to the card networks.

- Gateway / PSP: the secure front door that collects payment details and returns a result to your site, link, or app.

- Issuing bank: your customer’s bank. It decides to approve or decline.

- Card networks: the rails for cards. Examples include Visa and Mastercard.

- NAPS: Qatar’s national payments network that supports domestic cards across ATMs, POS, and online.

- QPAY: the online flow most domestic cardholders follow. Buyers enter an OTP by SMS, then confirm with their card PIN on the bank page.

- 3-D Secure: extra authentication on card payments. In Qatar, expect OTP then PIN.

- Apple Pay: a mobile wallet that lets buyers pay with a stored card on iOS. Treat it as a convenience layer.

- Statement descriptor: the label that appears on your customer’s bank statement. Keep it recognizable to reduce disputes.

- Soft decline: a temporary no. Often fixed by a retry or an extra piece of data.

- Hard decline: a firm no. Do not retry endlessly. Offer another method or a fresh link.

- Chargeback: a dispute opened by the issuing bank. You can submit evidence within a set window.

- Rolling reserve: a small percentage of your settlements that is held for a time to cover risk.

- Settlement: when funds from accepted payments arrive in your bank account.

- Payout report: the file that ties a settlement to the charges and refunds inside it. Use it for reconciliation.

- Tokenization: storing a secure token instead of raw card data so returning buyers can pay again.

- Webhooks: machine-to-machine notifications for events like paid, failed, or refunded. Treat them as your ledger of truth.

- MCC (Merchant Category Code): a four-digit code that describes your business type. It can affect fees and risk rules.

- AVS / CVC: address and card security checks that improve acceptance when available.

- Effective rate: your real, blended cost per transaction after all fees. This is the number finance should plan around.

Final words and next steps

You came here to choose a processor and get paid. SADAD fits the way small businesses in Qatar actually sell. Now make it real. Open your SADAD dashboard at SADAD.qa, create a payment link, share it on WhatsApp or email, and collect a live payment. One action, one receipt, proof you’re set.

Running WooCommerce or Shopify. Turn on the SADAD method, place a small mobile order, and confirm the success page and refund path. Your checkout stays on brand and respects the local OTP plus PIN flow.

If you want a walk-through, book a short session with the team. You’ll connect links, invoices, and your store in one sitting and leave with a verified money path. Head to developer.SADAD.qa for APIs, SDKs, and webhooks. Keep payment creation on the server, use tokenization for returning buyers, and wire up webhooks as your source of truth.

Make your first payment today. Add Apple Pay when your bank supports it. Layer WooCommerce or Shopify when the catalog is ready. The best processor is the one that moves cash now and scales when you do.

start from here

Last Articles

Articles

Your Phone Is a POS Terminal Now: The Complete Guide to Tap-to-Phone Payments in Qatar

Tap-to-Phone Payments in Qatar: Turn Your Phone Into a POS Terminal and Start Getting Paid Today Your customers are already tapping to pay. The real question is whether your business...

Read more

Articles

The Qatar Business Owner’s Guide to WhatsApp Commerce and Getting Paid Faster

WhatsApp Commerce in Qatar: How to Turn Conversations into Sales with Payment Links You have already made sales on WhatsApp without calling them sales. A customer messages you asking about...

Read more

Articles

SADAD 360: The All-in-One Business Suite Built for Qatar’s SMEs

SADAD 360: The All-in-One Business Suite Built for Qatar's SMEs Most businesses in Qatar aren't struggling because of bad products or poor service. They're struggling because they're running their operations...

Read more